How This TSP Millionaire Ran Out of Money

One of the most difficult parts about our job is watching retirees make mistakes in their retirement plan. We recently met with a family that came to us after managing their finances during their lives like most families. Not long ago, they had done some retirement planning and had a plan put together for them.

They brought this retirement plan to us, and it showed that they had roughly $1.7M at the time of creation. They weren’t doing poorly by any means.

But the reason they contacted us was because their new projections were showing that they were going to run out of money by age 78. They were confused about how they went from a $1.7M portfolio that seemed sustainable, to being in this economically dangerous position.

They were puzzled because they were great budgeters, so the common culprit—overspending—was not the issue this time.

What created such a change in their trajectory? In this article, we’re going to go over the three biggest contributors to putting them on this path, and strategies for each mistake that could have helped them avoid being in this position.

Sequence of Returns Risk

The first reason they were running out of money is because they did not address something called Sequence of Returns risk.

In short, it’s the risk that your investments could have less-favorable returns during the time that you need money from your portfolio, like in retirement. Let’s explore this together:

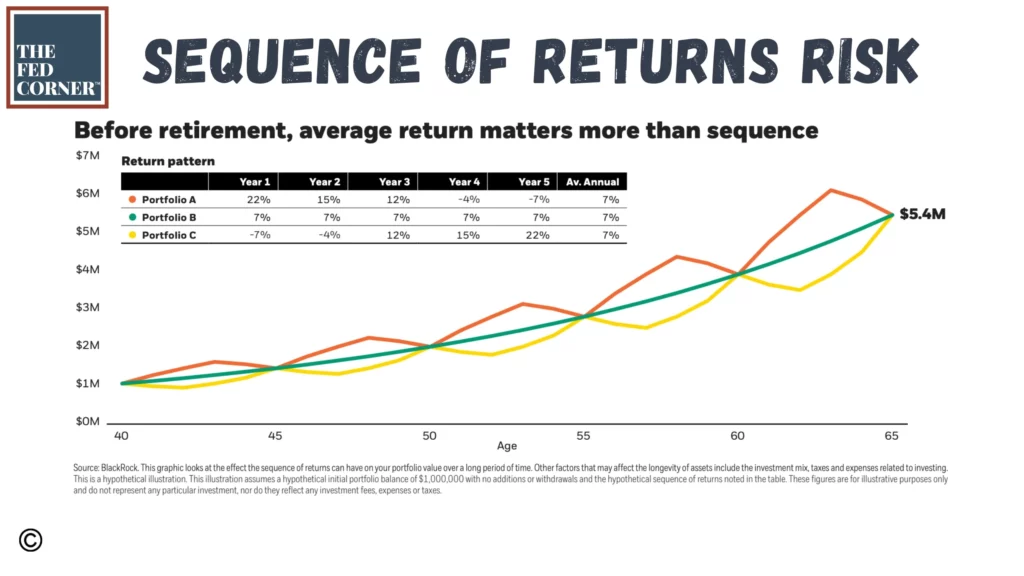

This graphic is a model from Blackrock, and it shows three portfolios that each have the same average annual return.

They each have a different sequenceof investment returns, but they all have the same average annual return. None of these portfolios have any money being taken from them, so this is like your TSP when you’re still working. You’re contributing and over time your balance is growing, according to how you’re invested.

In this model, you can see they all end up in just about the same place even though their paths were different. But that changes when you factor in withdrawals.

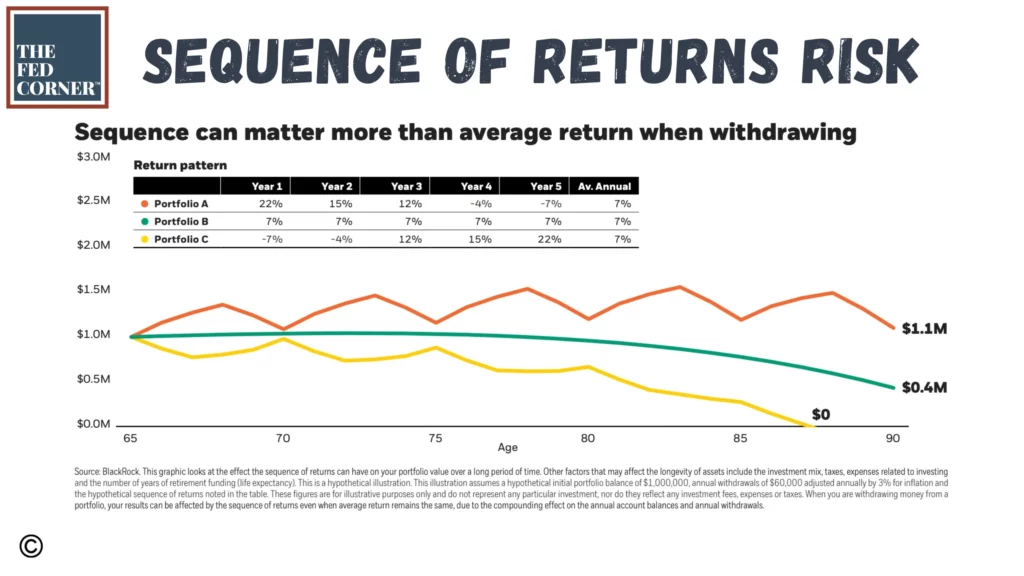

This next graphic has the exact same scenario as before, only now it factors in withdrawals. This is like how federal retirees take money from their portfolio to help pay for their retirement. This can also be RMDs when the IRS forces you to take out money out of your traditional or inherited retirement accounts.

You can see how having a different sequence of investment returns creates a risk that could completely deplete those assets much sooner than anticipated.

How could they have avoided this? This one is more challenging because you can’t control the markets. But like we always tell our clients, you can control how you participate in the markets.

If they had done some modeling, particularly one called Monte Carlo, they might have been able to see that their plan wasn’t sustainable. A Monte Carlo analysis is a form of financial modeling that shows probabilities of success by applying a specific scenario to 1000 various market returns. Doing this might have shown them that there was a significant amount of risk in how they were invested, and that challenging markets would have been more damaging than expected.

No TSP Distribution System

The next major contributing factor goes hand-in-hand with the first one. We noticed that they didn’t have a distribution system in place.

When you have a portfolio, it should be invested in various different kinds of stocks, bonds, international, money markets, etc. This is common knowledge.

When you decide to take money from your portfolio, should you distribute proportionally from your diversified assets, like the TSP handles withdrawals?

We’ve found that a better way of distributing money from your portfolio is going in and looking to see which investments are the most appropriate to generate the cash you need.

As with Sequence of Returns risk, you don’t want to sell investments that have fallen in value, because doing so means you took the money out of the markets and removed its chance of regrowing again. As a result, the massive market swings in 2020 and 2022 created significant risk to this family as they took distributions.

Instead, they may have been better suited by creating a system that identifies:

- How much income they needed per month

- How much time do they need this income—for instance, “we need $7K/mo for the next 4 years until Social Security begins”

- How to best allocate that needed $336,000 ($7K/mo X 12 months X 4 years)

- How to draw from it monthly over those 4 years

- What parts of their portfolio should that come from to minimizing the risk of making market volatility permanent losses

In addition to the above questions, there is also the factor of being the most tax-efficient when creating their retirement income. If not careful, a federal retiree can easily create more tax liabilities than are necessary, and that can hurt your retirement over time.

They should have identified which accounts made the most sense from which to make their withdrawals.

Perhaps a combination of retirement and non-retirement distributions is the best thing. Conversely, maybe it’s a low tax year and you should be taking all pre-tax retirement money and paying taxes while your rates are low. These are all things that get implemented through a distribution system.

This is where having projections of your income can be helpful. No one can know where tax rates will be in the future, but having a rough idea of what your expected income levels will be can help you figure out exactly how to use your money in a way that keeps taxes as low as possible throughout your life.

Poor Investment Plan

In addition to the prior, we immediately identified that they didn’t have a good plan around their investments.

Take a moment to think about how difficult the markets were last year. You’ll recall there was a big selloff in the markets. Neither stocks nor bonds were safe from volatility last year.

How many of you either did or were tempted to move your TSP to the G fund last year? How about in 2020 when COVID first hit, and everyone thought the world was ending?

Most current or soon-to-be retirees are trying to preserve their wealth, and many make financial moves without modeling or considering all the implications prior to doing so.

If you did too, or maybe you thought about it, where did that decision come from? It was visceral, right? You wanted to stop your account balance from further decline.

There has been a Nobel Prize won in behavioral economics. Managing your money successfully requires much more finesse than simple projections. It’s a careful blend of both science (modeling/math) and art (strategy/tactics).

If you moved to the G Fund after watching your TSP reduce by -10%, -15%, or more, did you get back into stocks before the markets took off again and recovered their decline? Chances are you didn’t, which means you took away the opportunity for your account to regrow again.

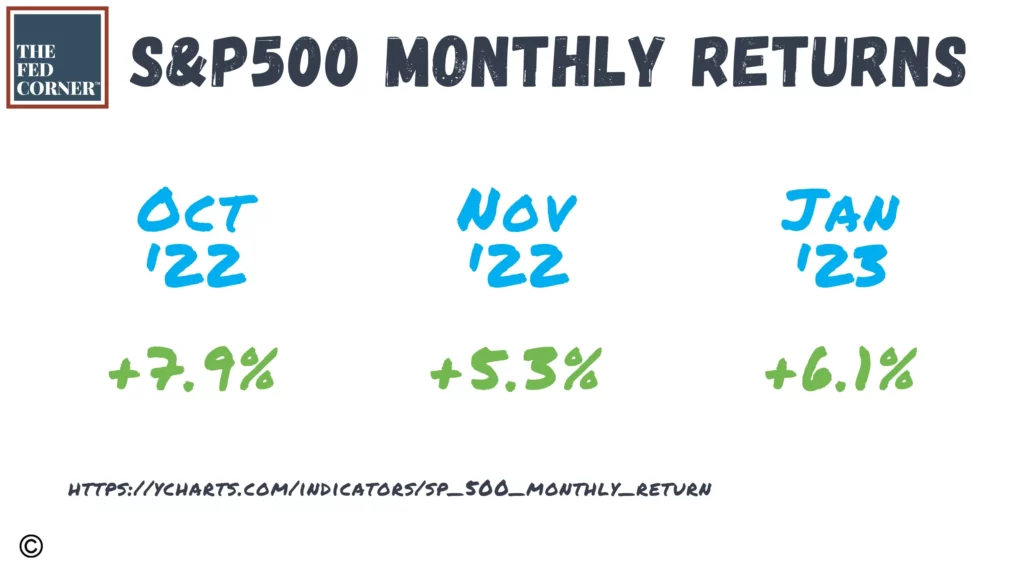

In October of 2022, the S&P grew by nearly 8%, then in November by around 5%, then in January of this year it grew again by around 6%, and if you were sheltered in more conservative investments like the G fund, you missed out on that return.

On the other hand, in December it lost almost 6%. We can clearly see the need for having an investment plan that’s going to help a retiree meet both their income needs, as well as their growth needs. Future-you will need inflation-adjusted income so that you can continue living the life that today-youis living.

Often, the total cost of retirement can be several millions of dollars over time, especially if living in more expensive areas like here near Washington, DC. While this is very lifestyle dependent, federal retirees need to make their savings last for longer than many realize.

Too much cash means they don’t keep up with inflation. Being too aggressive could mean that the sequence of their stock returns could impact their safety.

This family should have had an investment allocation that was appropriate for them and their goals, which was to stay financially independent in retirement.

They could have planned out how much income they needed in segments of 5 years or so, then started putting together a portfolio to help meet those income goals along the way.

How They Could Have Seen It Coming

The worst part is that this family could have prevented being in this position today if they had done some scenario planning.

Financial modeling can’t be guaranteed, but it gives you an extremely mathematically-accurate way of identifying whether your current financial position and plan are sustainable and helps identify future risks to your goals.

We’re very evidence-based in our firm, meaning that we believe goals-planning is fine and dandy, but there is nothing like running the full analyses, because the numbers don’t lie.

Creating what-if scenarios in a plan can help a family identify whether their financial position has any risks that could be coming down the line for them.

Some examples of helpful questions to ask and subsequently model:

- What if we spend $6,000/month instead of $4,000?

- What if inflation stays higher for longer?

- What if we stay this conservatively/aggressively invested?

- How much can we save in taxes with Roth conversions during our lives?

- What if we have an expensive health situation later in life, like a long-term care event?

- How do we fix our upcoming RMD problem?

Once you see the results of these scenarios, you can begin to work out strategies to help you prevent a situation that leads you towards an undesirable future. Remember, creating a plan is worthless unless you implement the actions that come from going through the exercise.

The first quarter of 2023 is nearly over. Take the time this year to identify and focus on the factors that move the needle in your wealth and do the planning your family deserves. After all it’s not just your money, it’s your future.

Categories

- FEGLI

- FERS Pension

- General Financial Planning

- Health Benefits (FEHB)

- Insurance and Estate

- Social Security

- Thrift Savings Plan (TSP)

Recent Posts

These Problems May Be Quietly Hiding in Your Tax Return

May 18, 2026

This “Drive-By” Planning Will Cost Retired Feds Thousands

Mar 17, 2026

ORA Debunked and Tips to Submit Your FERS Retirement

Jan 17, 2026