Debt Ceiling Limit and how it impacts the TSP G Fund

The federal government has exhausted its ability to borrow any more money at the risk of reaching its debit ceiling. Treasuries used to fund the G fund in the TSP have ceased to receive reinvestments.

At first look, this sounds terrifying and can cause a lot of doubt to federal employees. But we’re here to help you distinguish signal from noise and discuss why this is happening, what it means, and what you should do about it.

Understanding the Suspension

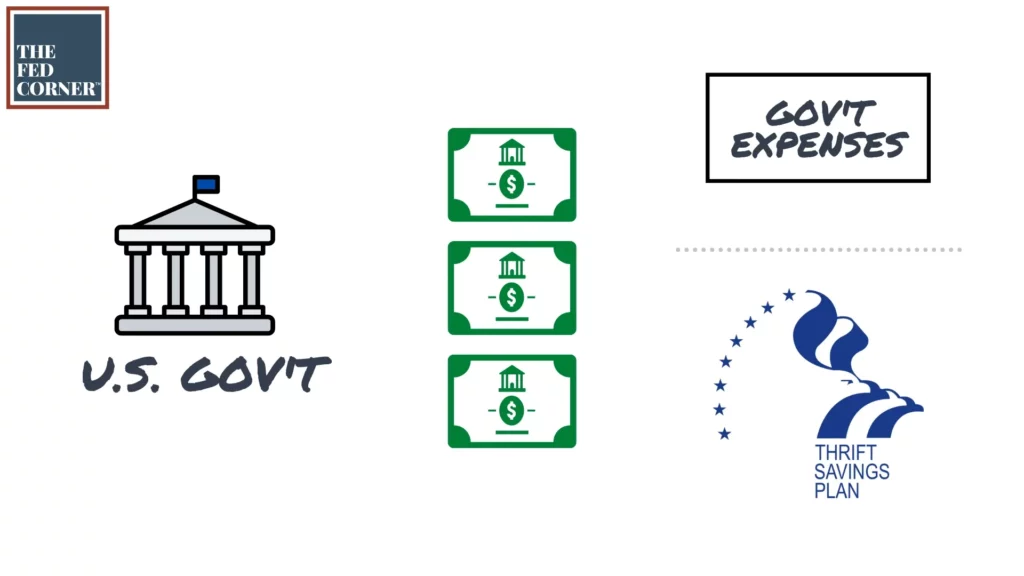

The TSP’s G Fund invests in short-term treasuries issued by the government to the TSP. Because of this, the G Fund can be affected when the debt limit is reached, which just happened recently. Watch the video for an explanation of how the graphic below works.

When the debt ceiling is reached, the Treasury looks for ways to manage its cash and borrowing to continue funding the government. One way it does this is by suspending investments of the G Fund, since continuing to fund it would cause the government to exceed its national debt limit.

U.S. law authorizes the Secretary of the Treasury to do this if investments can’t be made without going over the debt ceiling.

Here are some quotes from letters written by Yellen:

“As of January 23, I have also determined that, by reason of the statutory debt limit, I will be unable to fully invest the Government Securities Investment Fund (G Fund) of the Thrift Savings Fund, part of the Federal Employees’ Retirement System, in interest bearing securities of the United States…

While Treasury is not currently able to provide an estimate of how long extraordinary measures will enable us to continue to pay the government’s obligations, it is unlikely that cash and extraordinary measures will be exhausted before early June…” she wrote to Congressional leaders.”

We won’t discuss the politics surrounding this. Our objective is to help you feel confident and prepared for retirement from service, so next we’ll discuss how this translates to federal employees.

How Federal Employees are Impacted

In essence, TSP participants are helping to fund the operation of the federal government. This is because G Fund assets in the TSP will once again be used by the federal government to help meet expenses.

This sounds like they are taking your money, but the secretary of Treasury can’t actually sell or redeem Treasury Bonds help by TSP participants. However, they do have the ability to “suspend the issuance of additional amounts of obligations of the United States if such issuance could not be made without causing the public debt of the United States to exceed the public debt limit.”

Here’s the important part: once the government can handle the debt ceiling issue, either by suspending or increasing the limit, federal employees are “made whole” again. The G fund still earns the interest, just not in real time. Eventually, the Treasury will “pay back” the fund to make it as if it never happened. So, it’s basically like a big I.O.U.

Ordinarily, claims like this would be suspicious, however the full faith and credit of the United States federal government stand behinds this claim. Politics aside, this is the “safest” kind of debt investment (bond) that an investor can own. Understand that it’s the safest from volatility, but it’s not safe in helping you protect your financial independence throughout retirement.

That said, if the U.S. were to default on their debt payments, how would that impact U.S. Treasury Bonds and the G Fund? They are likely to suffer. Just recently, Fitch (one of the largest credit rating agencies) has put the U.S. on a downgrade watch list. This means they’re losing faith in the government’s ability to pay.

What Should Federal Employees Do?

Try to keep your nerves at bay. The worst thing you can do is make decisions about your money when you’re anxious or panicked. However, there are steps you can take to help insulate yourself from volatility.

Shameless plug: the first thing you can do is sign up for content designed to give you massive value and actionable ideas to help build your wealth. That’s our free newsletter. Our clients say they love our newsletter, and if you’re not on it yet, you’re missing out! Find it here.

You can still take money out of the TSP, and your money is still there. It’s not like it has vaporized.

In fact, we’ve been working with feds for a long time, and this isn’t the first time we’ve seen something like this. Our perspective is that you don’t need to worry about the G fund becoming illiquid any time soon. As such:

- You should not move all your money away from the G fund. Doing so to other TSP funds or the MFW can increase the risk in your portfolio, and if markets become volatile, you will see more volatility.

- You can and should continue to make TSP contributions if it fits within your retirement plan.

- You should not create additional market or interest rate risk by moving G fund assets into any of the other TSP funds, F, C, S, and I. Doing this increases various risks in your portfolio and should be done only within the confines of a proper investment plan.

The way that this challenge becomes a problem is if the government is no longer able to pay back its debt, meaning it defaults on its loans. The likelihood of the federal government defaulting and not being able to pay it back is low. The probability of this challenge becoming resolved is greater than any risk of staying in the G fund.

But at the same time, we know it’s frustrating to feel like they are commandeering your money and that you have no control. Retirement planning is all about creating options for yourself so that you can have the confidence in your future, and we understand that this event may cause anxiety rather than confidence.

One way that federal employees can help do this is by diversifying their conservative positions. Right now, with interest rates where they are, there is massive opportunities in the bond markets to capture higher yields for 1, 2, 3, or even more years. Bond ladders have become an extremely valuable strategy for retirees as a way to conservatively invest but still earn a respectable yield back to their portfolios. Cashflow is the heartbeat of a retirement plan, and setting up your wealth appropriately is imperative.

Want a Little Help?

And so, we’d like to extend ourselves as a sounding board to you. Ordinarily, as a private firm, we’re not able to work with everyone that comes our way. But we understand there are a lot of federal employees that are truly scared right now, and we want to help however we can.

If you want to talk to one of our advisors, we’re happy to give you some of our time. We’re offering brief, 10–15-minute phone calls at no charge whatsoever, to help offer some perspective.

Legal will be upset with me if I don’t remind you to please understand that we will not be able to speak with everyone, and this is subject to availability of our team. Please also understand that what we discuss is not considered advice unless we are working together on an official capacity.

I hope this helps answer questions, and if you’re a federal employee planning your retirement, consider subscribing to our YouTube channel to see our videos about how to plan a better retirement, because it’s not just your money, it’s your future.

Categories

- FEGLI

- FERS Pension

- General Financial Planning

- Health Benefits (FEHB)

- Insurance and Estate

- Social Security

- Thrift Savings Plan (TSP)

Recent Posts

This “Drive-By” Planning Will Cost Retired Feds Thousands

Mar 17, 2026

ORA Debunked and Tips to Submit Your FERS Retirement

Jan 17, 2026

New TSP Rules Every Federal Employee Needs to Plan For (2026 Strategy Guide)

Oct 29, 2025